")

Pitch

Fossil fuel companies set aside the revenue raised from a price on carbon and use it to gain market share in low carbon energy generation.

Description

Summary

Environmentalists are demanding a tax or fee be paid by the fossil fuel industry as a way to combat climate change. However, the conservatives in the U.S. Congress point out that this would increase the cost of energy, putting U.S. companies at a competitive disadvantage, sending jobs overseas.

This deadlock has changed little over the past three decades and all the while we continue to increase the concentration of carbon dioxide in our atmosphere.

Like most solutions, it lies somewhere between. What is needed is a price on carbon to reduce carbon emissions at no overall cost to a fossil fuel industry transitioning to a low carbon future.

The answer is an Internalised Price on Carbon (IPC).

The fossil fuel industry will ask the government to apply a rising price-on-carbon on each energy company, where the revenue raised is recycled back by that energy company as different revenue streams, for different source types of energy, relative to how much energy each source type generates or is expected to generate.

This would put low carbon energy at an advantage because, though each energy type would receive an equal share of the revenue relative to the amount of energy generated or expected to be generated, low carbon energy will pay little or nothing towards raising this revenue (from carbon) in the first place.

A simplified example would be, an oil company which wants to diversify into nuclear. It uses the revenue it raises through having to pay a price on carbon, to subsidise its nuclear ambitions.

This solution will allow energy companies to diversify into technologies which are lower yielding and presently slightly more expensive than fossil fuels, without losing market share because all companies will have to transition to a low carbon future together.

The increase in energy prices in real terms will only be about 1.5% p.a. A small price to pay to keep the atmosphere stable for future generations.

Category of the action

Mitigation - Helping U.S. enact carbon price legislation

What actions do you propose?

Recycled Revenue.

That the fossil fuel industry in the U.S. will be asked to consider a price on carbon of U.S. $5.00 / tonne, rising at a rate of U.S. $5.00 per annum. However, the revenue raised by each individual company will then be divided up, ring-fenced, and returned back to that company as a subsidy for each individual energy source type. The value of each subsidy will be proportional to the amount of energy generated (or to be generated) by that source type, and will bear no relationship to the quantity of carbon emissions. However, because the initial carbon revenue raised will be paid in proportion to the amount of carbon, high carbon energy will become increasingly uncompetitive.

It may be the case that some fossil fuel companies may not want to diversify into low carbon energy, but lets look at what is being offered here. A fossil fuel company given the choice between paying the revenue raised through a price on carbon to the government, taxpayer or citizens, compared with investing it in its own low carbon energy ventures, would definitely choose the latter. The fossil fuel industry will literally save trillions of dollars by accepting this Internalised Price on Carbon (IPC). The carbon revenue raised by any company will be invested back into that company. None of the carbon revenue raised will leave the company.

If the fossil fuel industry collectively accept an IPC, there will be no need for the fossil fuel industry or the public to pay carbon taxes, no need for the fossil fuel industry to pay carbon dividends to citizens, and no need for any industry to pay for carbon emissions permits.

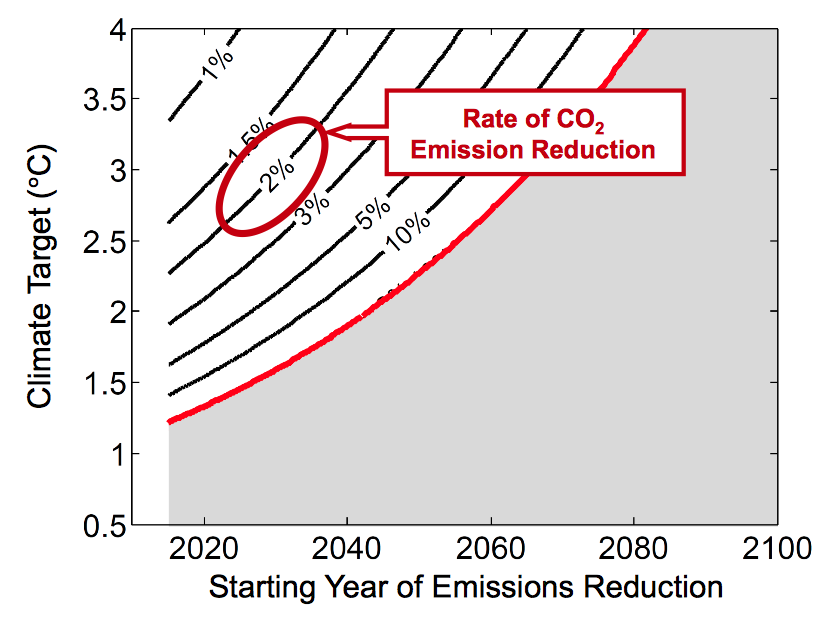

An IPC, will increase the price of fossil fuels, but unlike a carbon tax, will reduce the price of low carbon energy. For the sake of this presentation, a model is used which shows nuclear and wind becoming cost competitive with oil around 2040. Before this date, there will still be little cost incentive for both end users and utilities companies to purchase low carbon energy. Therefore, to get fossil fuel companies to diversify it will be necessary for them to abide to a CO2 emissions reduction standard of about 2% per year. After 2040, the demand for low carbon energy will be greater than for fossil fuels, so those companies who are able to supply low carbon energy will become the market leaders.

Emissions Reduction Standard.

To get the fossil fuel companies to abide to a CO2 emissions reduction standard of about 2% per year (0.17% per month), a penalty should be introduced. A fossil fuel company which fails to meet the monthly target would forfeit it’s carbon revenue raised for that month. This revenue would instead be distributed to all the other energy companies in the scheme on a per unit of energy generated basis. Notice that no revenue leaves the energy sector. Because this penalty carbon revenue will be raised in proportion to the amount of carbon passing through the offending company, but will be distributed on a per unit of energy generated basis, the overall direction of revenue flow will be towards subsidising low carbon energy at the expense of fossil fuels.

Even though energy companies will be opening themselves up to the risk of being penalised for failing to meet their monthly CO2 emissions reduction target, the risks will be outweighed through the possibility of receiving revenue from other companies which fail to cut their CO2e emissions.

Ring Fencing.

For an IPC scheme to work, energy companies will need to be split up into departments depending on the sources of energy. The departments will need to be financially ringfenced to ensure that the carbon revenue raised is redistributed within each company solely on a per unit of energy basis, so that revenue due to be paid to a low carbon generation department cannot find it’s way back to a fossil fuel department. A committee could be set up to audit this, with the administration costs being taken from the carbon revenue.

Once the scheme is started, it'll be in the fossil fuel companies interest to ensure it doesn't fail. A failure in carbon price would delay low carbon energy becoming cost competitive with fossil fuels, making any investment into low carbon technology by the fossil fuel industry worthless. Because the financial fallout would be catastrophic the fossil fuel industry would also want to audit each other's books, to insure against widespread cheating which could bring the system down.

It will not be necessary for government to impose restrictions on markup. Companies will be unable to offset the carbon price signal by manipulating the profit margin. Market forces (competition between energy companies) will still be the determining factor for energy companies deciding on how much margin to apply to the individual energy types.

Ensuring Low Carbon Investment.

The US Department of Energy would need to ensure that the fossil fuel companies were investing the carbon revenue in low carbon energy generation. They could achieve this in three ways.

-

Ensuring the companies are adhering to the 2% Emissions Reduction Standard.

-

Ensuring the different types of energy generation departments in each company are clearly ring fenced, with departments invoicing services from each other.

-

If possible, each department should be set up as a separate tax entity.

Initially, the 2% Emissions Reduction Standard per year would ensure that more and more energy would have to be produced from low carbon generation. Secondly, because each ring fenced energy department would be responsible for maximising its own profit, low carbon generation departments would ensure that they receive all the carbon revenue that they are due. Thirdly, the Department of Energy would be able to cross reference invoices filed for tax purposes.

Enforcement to prevent windfall profits.

As discussed in the “Impacts” section below, it is inevitable that the fossil fuel companies will pass on some of the costs of raising the carbon revenue to the consumers. If the fossil fuel companies were then just to keep the carbon revenue, instead of reinvesting it into low carbon energy generation, this would be an easy windfall profit.

The 2% Emissions Reduction Standard per year (ERS) would prevent energy companies from making this windfall profit. Initially, the carbon revenue raised would be small, and the cost of adhering to the 2% ERS would be greater than this. However, once the low carbon energy becomes cost competitive, the fossil fuel departments would have great difficulty passing on the carbon revenue costs because of the competition from low carbon energy.

Finance

The investment required to transition to a low carbon economy is like nothing seen in history to date. It will not be possible to attract this investment without a price on carbon giving low carbon energy a competitive advantage. Full bipartisan support for a rising price on carbon is just one of the guarantees needed by financial institutions to reduce risk and offer cheap finance. Financial institutions cannot just demand higher interest rates to offset the risks. A high cost of finance heavily increases system levelised costs, making energy unaffordable in the long run, increasing risks further.

Even confidence in the energy market is only one side of the coin. What isn’t so appreciated is that the energy industry will still have to compete for investment capital from other sectors of the market, especially the residential property market. Despite the sub-prime housing crisis, financial institutions still favour investing in the housing market rather than new industrial projects. This is because a house acts as collateral reducing risk against a loan. Therefore, financial institutions have very little interest in investing in new industrial projects without charging high interest rates.

A small change in monetary policy would save the energy industry trillions of dollars in financing the transition to a low carbon economy. Financial institutions (banks etc,) should be prevented from making loans to the residential sector by using ‘promises to pay back those loans’ on the assets side of their balance sheets. Such loans should be made from real bank deposits. This would redirect trillions of dollars of investment revenue from the housing market (which does nothing but push up property prices) to the industrial sector, which urgently needs massive investment to decarbonise. The energy industry definitely have the clout to demand such a change, but are probably unaware that speculative investment into the housing market, pushes up interest rates, reduces the value of money without adding any value to the economy.

Follow the link to the Bank of England to see how money is created in a modern economy: http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/2014/qb14q1prereleasemoneycreation.pdf

Reducing the cost of finance, and thus reducing low carbon system levelised costs means that low carbon energy can become cost competitive earlier. Another way to reduce the cost of finance would be through a green bank. (See REFERENCES below.)

The pros and cons of an Internalised Price on Carbon (IPC) compared to other carbon pricing instruments.

The pros:

-

100% of the revenue raised is used to help the fossil fuel industry diversify into low carbon energy.

-

Directly reduces the costs of low carbon energy.

-

Does not transfer, what the fossil fuel industry consider to be ‘hard earned profits’ to their competitors in the low carbon energy sector.

-

The carbon revenue raised will give the fossil fuel industry a clear competitive advantage when they diversify into the low carbon energy market.

The cons:

-

No tax rebates or dividends paid to the public.

-

Without proper auditing, there could be carbon leakage, meaning that most of the revenue raised through a price on carbon may find it’s way back to the fossil fuel sector.

-

CO2 emissions reduction standards would still be required to encourage the fossil fuel industry to expand its portfolio into low carbon energy.

-

Raises no revenue for the government.

Additional Impacts to Consumers.

The impacts to consumers under an IPC would be much smaller than the impacts under present policy. Today, the government subsidies for low carbon ventures is paid for by taxpayers and not the fossil fuel industry. Under an IPC, the fossil fuel companies will subsidise alternative energy with the revenue raised through the price on carbon.

Much of the costs the fossil fuel industry will have to pay for a price on carbon and the costs of having to abide to the 2% Emissions Reduction Standard will be passed on to consumers, but this increase in fossil fuel energy prices will be less than the extra taxes the public would have to pay if the government continues to subsidise low carbon energy. This is because the fossil fuel departments will be limited into how much they will be able to increase the price of fossil fuel energy, due to direct competition from a steadily decreasing price of low carbon energy.

UNVERIFIED ASSUMPTION

Oil costs in this proposal are for the transport sector only. It is highly unlikely that oil will be burnt in new power plants after 2020, but will continue to be used for the transportation sector.

‘Well to wheel’ energy capital costs for internal combustion engine vehicles (ICEs) may be lower than for electric vehicles (EVs) running on electricity generated from natural gas. Firstly, ICEs are cheaper to build than EVs. Secondly, capital costs for building a national recharging infrastructure will have to be taken into account. (These higher capital cost may be the reason for the slow uptake of EVs to date.)

For the sake of simplicity, this proposal attempts to reflect this by reducing the system levelised cost of oil. Strictly speaking, this is incorrect and more complex accounting is required, but is beyond the remit of this proposal. However, even if system levelised costs for oil are higher, low carbon energy will become cost competitive earlier than the model used in this proposal.

Who will take these actions?

A team of energy economists would need to write a flexible application, which fossil fuel companies would be able to use to model their transition to a low carbon future using an IPC with CO2e emissions reduction standards.

Some fossil fuel CEO’s have already been calling for a pigovian tax on carbon, so analysis showing how much fossil fuel companies may save by recycling the price on carbon rather than paying it as a tax could very well act as the catalyst to get a price on carbon legislated.

It may turn out that the fossil fuel industry will lobby government for an IPC. A diversified fossil fuel industry will be decades ahead in reducing renewable energy prices to below fossil fuel energy prices compared with low carbon energy companies outside an IPC scheme. Companies outside the IPC scheme will clearly not be able to compete on cost if they are not receiving a carbon revenue subsidy. The fossil fuel industry will then be able to buy them up for two-a-penny, bring them within the IPC scheme and end up dominating low carbon market share. No doubt the Democrats will cry foul!

Once an IPC is put in place, it’ll mainly be the fossil fuel companies that import or extract fossil fuels which will join the scheme. These companies will be responsible for recycling the price on carbon, and diversifying into low carbon energy. However, the IPC could be applied anywhere along the supply chain, provided every tonne of carbon is accounted for, and no tonne of carbon is counted twice. If there is more than one company along the supply chain, then the long term survival of each company will depend on diversification, in which case the carbon price could be split between the companies.

Monitoring & Policing Activity

The fossil fuel companies will set up a committee to enforce self regulation, under the auspices of the US Department of Energy. Administration costs would be paid for from the carbon revenues. A company not adhering to regulation would forfeit some of its carbon revenue.

Where will these actions be taken?

The U.S. fossil fuel industry will request economists at American universities to develop flexible software, which individual fossil fuel companies will be able to use to model their transition to a low carbon future under an IPC. Because the transition to low carbon will differ greatly from company to company, and yet all companies will transition together creating an aggregate effect, the modelling would need to take into consideration both local microeconomic factors, as well as macroeconomics.

The fossil fuel companies who would use the software applications would be the national and multinationals operating within the U.S.A. as well as energy companies operating overseas wanting to retain market share, as the world transitions to a greener future.

Major international financial institutions will have to be consulted to ensure their backing.

Legislation would have to be at a federal level. As long as fossil fuels are cheaper than low carbon generation, state legislation would result in energy and energy intensive companies migrating to states without IPC legislation. Not only would this result in an increase in carbon emissions, but more importantly, would put pressure on state governors to delay action on climate change.

Taking the Initiative

An IPC is the only carbon pricing tool which ensures a healthy future for today's major energy firms. All other carbon pricing tools are specifically designed to mitigate climate change by killing off the fossil fuel industry by making it uncompetitive, and removing the very revenue required for it to transition to low carbon energy generation. No consideration has been given to the millions of workers who will lose their jobs or the health of the pension companies with investment portfolios in the major energy firms.

It is the U.S. fossil fuel industry which must take the initiative to get an IPC adopted. An IPC will be more politically acceptable in the US than the command and control response favoured by the EPA.

How much will emissions be reduced or sequestered vs. business as usual levels?

The following estimate is based on a model energy company “Best Energy Company”, importing oil and natural gas, (6000 and 4000 GWh/month equivalent, respectively), which diversifies into wind and nuclear generation (2300 and 7700 GWh/month, respectively) over a period of 60 years.

(See video presentation)

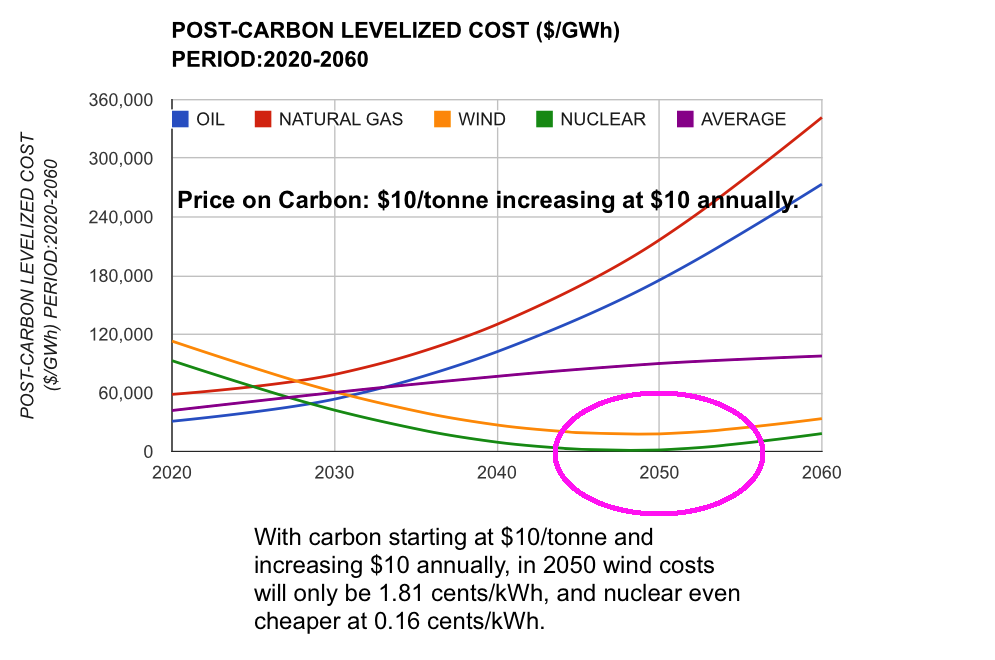

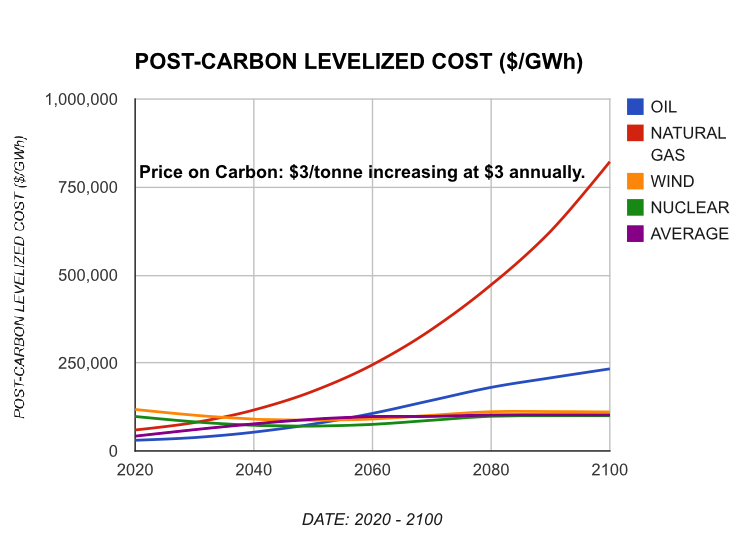

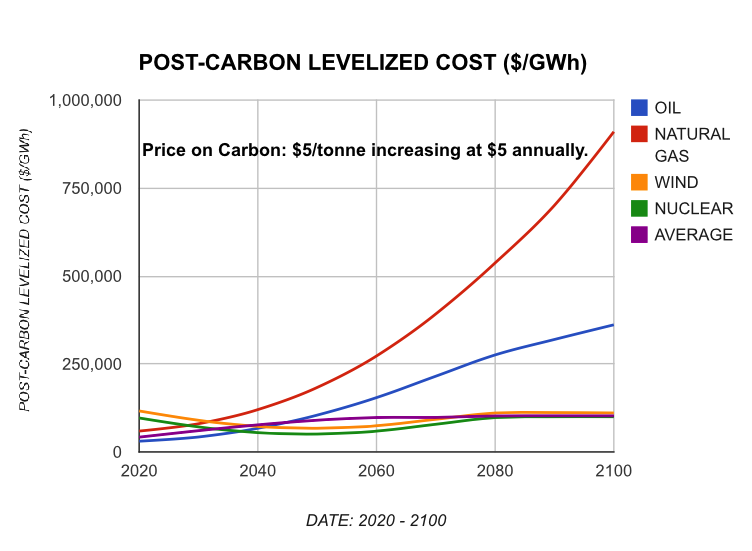

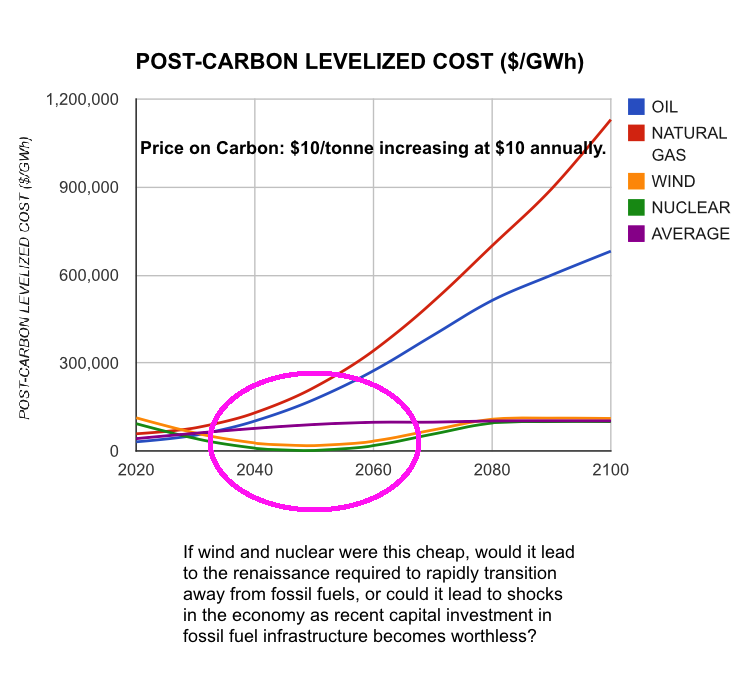

At a carbon price of U.S. $5.00 / tonne, rising at U.S. $5.00 per annum, starting in 2020, Best Energy Company’s energy generation could nearly be carbon free by 2080. That’s a carbon emissions reduction rate of 7.74% per year. (By comparison, the emissions reduction trajectory required to avoid a global average temperature rise of 2°C will be between 3% and 5% per year, by 2020 - Stocker 2013).

In essence, after low carbon energy becomes the competitive choice, the rate of emissions reductions will only be limited by how quickly low carbon generation can be built.

The model assumes Total System Levelized Cost as estimated by the US Department of Energy.

What are other key benefits?

1. None of the revenue raised by a price on carbon will be used to subsidise the competition, giving the fossil fuel industries’ new low carbon portfolios a clear advantage over low carbon energy generation outside the scheme.

2. Fossil fuel companies will not need to go out of business, but will transform themselves into energy companies, and diversify into low carbon energy. This means Fossil fuel companies will be able to retain and retrain their workforce, rather than there being mass redundancies as we transition to a low carbon future.

3. A spur in economic and industrial activity as energy companies prepare for cost competitive low carbon energy (due to the IPC).

4. Border rebates on exports and border tariffs on imports will need to be applied when trading with countries which fail to put a price on carbon. This will be a way of persuading those countries to also accept an IPC.

What are the proposal’s costs?

Using the model and carbon price above:

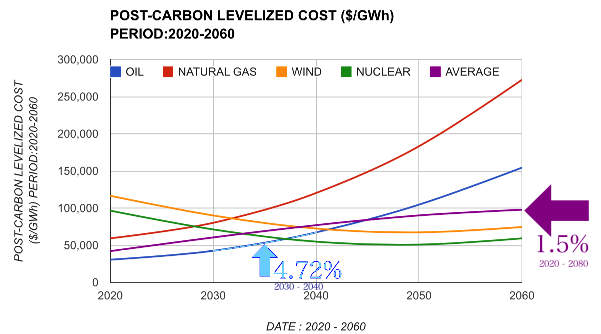

If Best Energy Company starts the scheme in 2020, its increase in energy costs (in year2020dollars) during the 2020 and 2080 period would be 1.50% per year. However, for a short period between 2030 and 2040 oil costs are shown to rise at 4.72% per year.

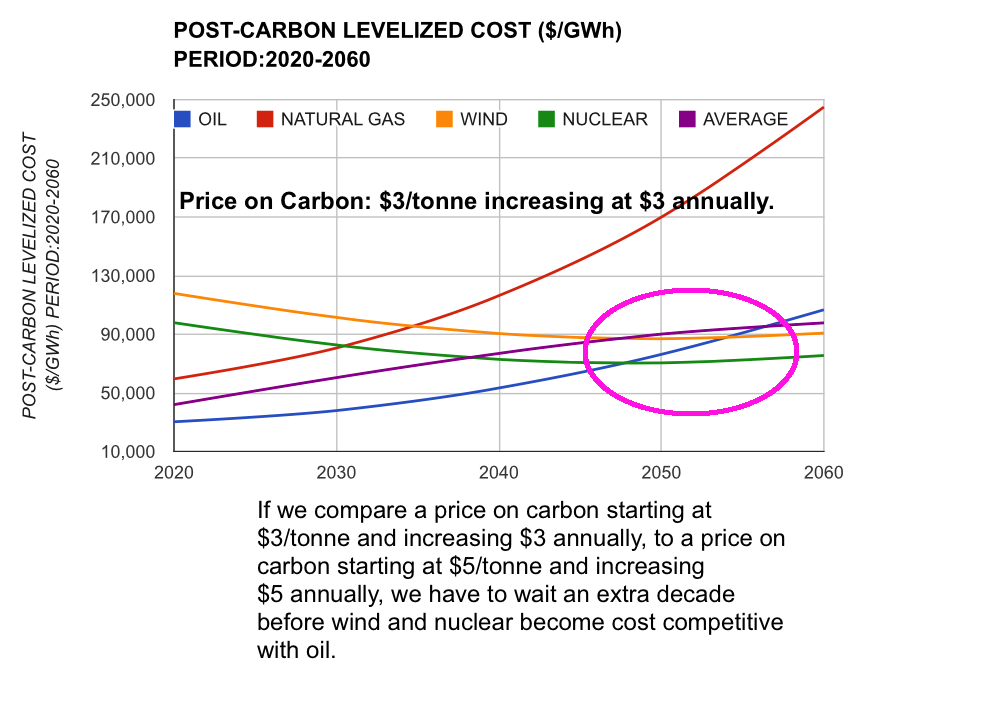

By comparison, the U.S. Energy Information Administration forecasts average fossil fuel prices to rise at about 2.44% per year, between 2013 and 2035.

The carbon cost will be applied to the Total System Levelized Costs, but because the carbon costs also act as a subsidy for low carbon generation, the overall carbon cost will be zero. In other words, the increase in price of energy will totally depend on how quickly technology can reduce the costs for low carbon generation, but during the transition period, the carbon revenue will buffer the increases in low carbon generation costs, as the model clearly demonstrates.

From an energy company’s point of view, because all energy companies will be transitioning to low carbon together, companies will be able to pass the costs on to the utilities companies and end users without losing market share.

Total System Levelized Costs could further be reduced by the formation of a ‘green bank’ and changes in monetary policy. See references below.

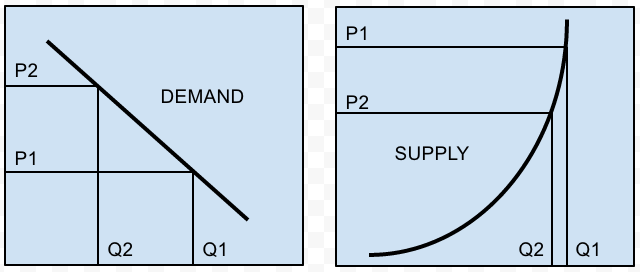

Supply Side Economics vs Costs to Consumers

In the demand curve, we can see that a carbon price will reduce the quantity of fossil fuels consumed, however, because the fossil fuel industry is finding it increasingly difficult to keep up with demand (see steep supply curve), any decrease in quantity of fossil fuels consumed will disproportionately dampen the original fossil fuel energy price increase.

Because an IPC results in a reduction in alternative energy prices as well as an increase in fossil fuel prices, this dampening effect will be less prominent in preventing low carbon energy from becoming competitive compared to other carbon pricing tools. Further, this will also reduce the impact to consumers.

Time line

Preparation.

2015: A team of consultants is put together to plan and oversee the implementation of an IPC. Energy economists prepare the software and use it to draw up a handful of emissions reduction scenarios.

2016: Fossil fuel companies use the software to plan and optimise their own carbon emissions reduction pathways . A platform is created where all parties can discuss their findings and ensure a level playing field. New low carbon business plans are drawn up by the fossil fuel industry.

2017: Financial institutions carry out risk/benefits analysis comparing a possible future where fossil fuel companies lose major capital through having to pay a price on carbon, compared with the certainty of fossil fuel companies reinvesting such capital through an IPC.

2018: Fossil fuel companies use their influence to get a bill passed through government, legislating an IPC.

2019: Fossil fuel companies financially ring fence their departments to ensure that the departments can not subsidise each other. A national committee is formed with a remit to audit the fossil fuel companies financial and carbon accounts.

2020: The scheme commences.

Low Carbon Phase in.

Ultimately, there will be many factors determining the rate of emissions reduction through the rest of this century. One of the limiting factors will be the rate and duration of energy price increases that society will accept. These are both dependant on the quantitative price on carbon.

Using the IPC model for Best Energy Company, the following plots demonstrate the rate of increase in system levelised costs and how long it will take before low carbon energy becomes cost competitive. A market led phase in of low carbon energy generation cannot get underway while fossil fuel energy generation is cheaper.

Plots between 2020 - 2060

Related proposals

The most closely related proposal to an Internalised Price on Carbon (IPC) is the Fee and Dividend solution by Citizens Climate Lobby - The Little Engine That Could.

The authors of this proposal are Peter Joseph, M.D. and Gary Horvitz, and I would like to take this opportunity to express my gratitude to all the hard work they do in advocacy.

A few times in their proposal they mention “politicians don’t create political will -- they respond to it.” and in a similar vein they discuss a “critical mass of civil society” becoming aware of the Fee and Dividend solution.

There will never be a "publicly driven political will" or a "critical mass" reached, and it can be demonstrated with Google Trends. Please watch my one-minute YouTube presentation demonstrating this point.

https://www.youtube.com/watch?v=lyqpWEF5cLw

We must not be in denial of how little interest there is in climate change.

We must start the hard and thankless task of negotiating with the fossil fuel companies.

References

An Internalised Price on Carbon (IPC) Video Link

An Internalised Price on Carbon (IPC) Spreadsheet Link

An Internalised Price on Carbon (IPC) PDF Spreadsheet

An Internalised Price on Carbon (IPC) This Document

Levelised Costs.

Approximations from the US Department of Energy have been used to estimate the Total System Levelized Costs. However, actual costs will vary according to location: http://www.eia.gov/forecasts/aeo/pdf/electricity_generation.pdf

A Green Bank

To reduce Total System Levelized Costs, a government ‘green bank’ must be setup to allow fossil fuel companies to obtain cheap finance. Such a government green bank will raise the finance required by using new loans to balance the asset side of its balance sheet. Follow link to see how money is created in a modern economy:

http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/2014/qb14q1prereleasemoneycreation.pdf

Double Accounting

The spreadsheet model assumes the carbon intensity for nuclear and renewables to be considered as zero for accounting purposes. This is despite real world carbon intensity for nuclear and renewables being about 30 tonnes of CO2e/GWh. The reason for this is because the embedded energy for nuclear and renewables has already had a carbon price added. For example, the digger used to mine the uranium consumes diesel. The price on carbon will already have been applied to the diesel, so if we applied a price on carbon for nuclear, it means the price would be applied twice.

Embedded Carbon

On initial consideration, it might seem that an equal subsidy is being handed to each type of low carbon generation despite some types of low carbon generation being more efficient than others, however this is not the case. The price on carbon will penalise low carbon energy with high embedded carbon. A good example of this is biofuels. The carbon price will increase the price of diesel used to run the tractors which harvest the biofuel crops. This will make biofuels more expensive and less competitive. A high price on carbon means that it will be more expensive to run a car on biodiesel than an electric car running on electricity generated from nuclear. The point is the price signal sets the market and the market chooses the winners.

Practical Considerations

In no way is this proposal favouring one type of low carbon energy over another. Each energy company will need to carry out it’s own analysis. What is promising to see, is that onshore wind could become cost competitive with fossil fuel energy at about the same time as nuclear, however there are many more considerations to take into account other than financial. A good start would be: http://www.withouthotair.com/download.html

Bridging Fuel

Likewise, this spreadsheet model indicates that natural gas would be a viable transition fuel until low carbon energy becomes cost competitive. However the model doesn’t take into account methane leakage through fracking: http://link.springer.com/article/10.1007/s10584-012-0401-0#page-1